A Micro-Cap Real Estate Gem Set for Triple-Digit Growth

CHCI is a hidden gem in the micro-cap space, set for 100%+ growth. With a capital-light model, over 60% insider ownership, and a compelling valuation of just 11.5x recurring earnings (or just 4.5x when factoring in guaranteed revenue/incentive fees) It represents a rare and overlooked opportunity in real estate management.

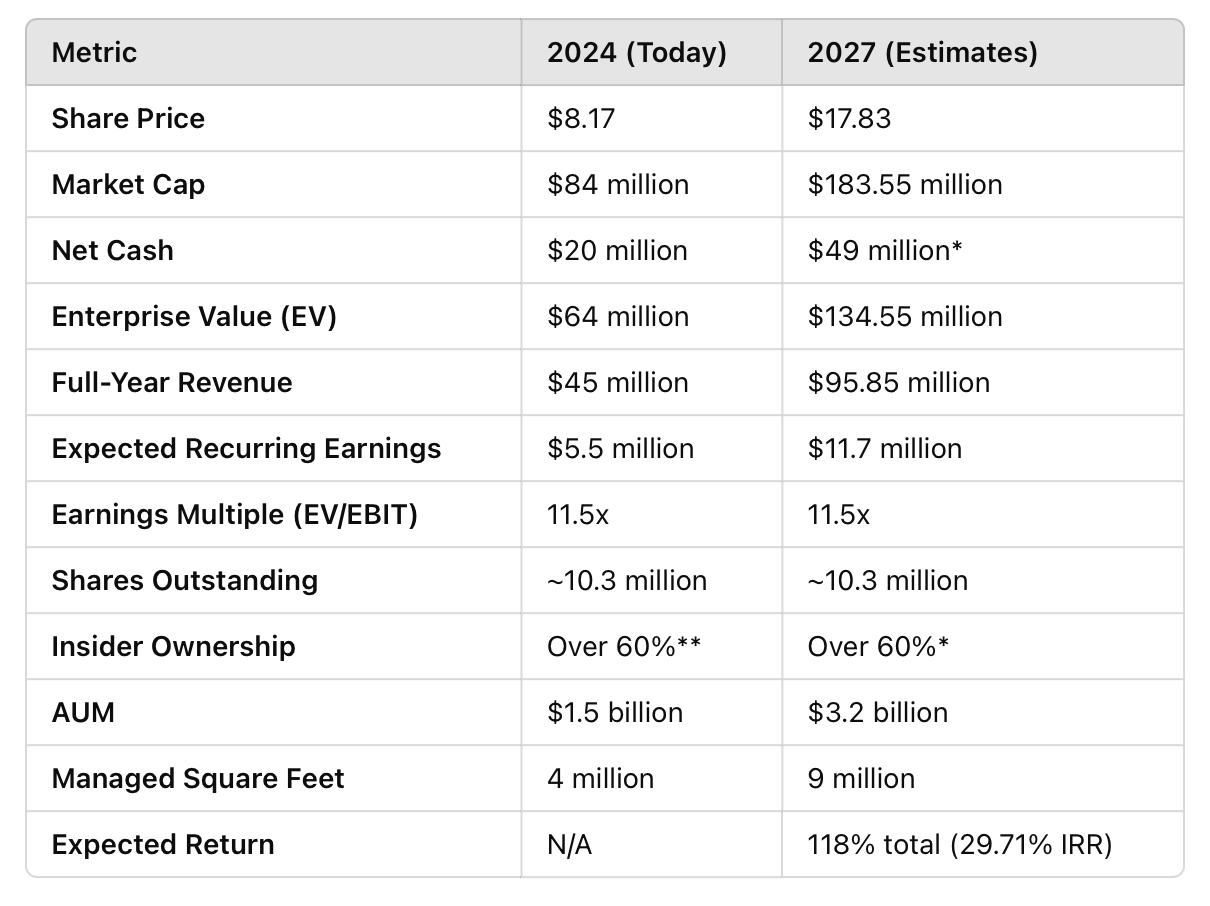

Quick snapshot of financials/valuation:

* Includes 3 yrs cash build and incentive fees

** 30% each by Dwight Schar and CEO

At first glance, Comstock Holding Companies (CHCI) appears reasonably priced at $8.17 per share. With $20 million in net cash, its enterprise value is just $64 million. Recurring earnings in 2024 are expected to reach $5.5 million, implying a valuation of 11.5x earnings.

For a micro-cap real estate management company, a multiple of 11.5x doesn’t initially seem particularly exciting. Some might even argue it’s too expensive given CHCI’s relatively illiquid status. However, upon closer inspection, there are compelling aspects to this story that warrant a deeper dive.

Management Alignment and a Legendary Investor

One of the most intriguing aspects of CHCI is management’s ownership of over 60% of outstanding shares. This level of insider ownership signals strong alignment with shareholders. What’s even more exciting is that Dwight Schar, the founder of the legendary homebuilder NVR, owns a 30% stake in CHCI. For context, NVR pioneered a capital-light homebuilding model that resulted in a staggering 180x increase in its stock price since 2000. CHCI’s CEO, Christopher Clemente, owns an additional 30% stake, reinforcing the alignment of interests.

CHCI operates with a similar capital-light model. Rather than owning real estate, CHCI acts as a manager, collecting fees based on the revenue generated by the properties it oversees. This approach allows the company to participate in real estate appreciation while minimizing the downside risks/capex typically associated with building out properties. Notably, nearly all properties managed by CHCI are owned in a 50/50 partnership between Clemente and Schar, creating a unique setup where they effectively pay CHCI to manage their own private real estate portfolio.

This is a helpful breakdown of the unique corporate structure :

CHCI currently manages 4 million square feet of real estate, representing $1.5 billion in assets under management (AUM). According to the most recent investor presentation, an additional 5 million square feet is either under development or in the pipeline, translating to $3.2 billion in AUM. This expansion is expected to largely materialize by the end of 2026, representing a 113% increase in AUM. The whole thesis can basically be explained with this one screenshot taken directly from Comstocks website :

The Chart below from the 2024 investor presentation is an in depth breakdown of the 5 million square feet of property currently being developed and in the pipeline for completion by 2026:

Assuming margins remain consistent and there is no operating leverage (a conservative assumption), CHCI would effectively be trading at just 5.5x earnings by 2026. However, the story doesn’t end there. Embedded within CHCI’s business model are several “free call options” that could add substantial upside.

Hidden “Free Call Options”

ParkX - Parking Management Business

ParkX operates as a subsidiary of CHCI and has seen explosive growth of 75% this year, with a 2024 annualized revenue run rate of $9.5 million.

Over 40% of ParkX’s contracts are with properties outside CHCI’s core Anchor Portfolio, offering uncapped growth potential.

The expansion into adjacent services, such as security, provides additional upside.

Venture Platform

Through its Venture Platform, CHCI makes small, low-risk capital investments that yield development fees and long-term management contracts.

Example: A $1.5 million land investment is projected to return the full investment, generate development fees, and secure property management rights. These investments are made with pre-arranged partnerships, minimizing risk.

Incentive Fees

In 2023, CHCI earned $4.8 million in incentive fees from triggering events on three assets. In 2024, an incentive fee tied to seven commercial assets was deferred.

Assuming similar metrics, the deferred fees could amount to approximately $11 million, expected no later than 2027. Factoring this into valuation reduces CHCI’s enterprise value to $53 million and its earnings multiple to just 4.5x.

Strategic Positioning in High-Value Real Estate Markets

Approximately 50% of CHCI’s managed assets are in commercial real estate, but potential sector concerns are mitigated by:

Strategic Location: Northern Virginia’s proximity to economic hubs and federal institutions creates consistent demand for high-quality properties.

Improved Connectivity: The Silver Line Metro expansion enhances access to Reston, Dulles Airport, and Loudoun County.

Supportive Land Use Plans: High-density, mixed-use developments near metro stations are encouraged by local policies.

Impressive List Of Tenants Including:

High Occupancy Rates

Commercial Properties: 94% leased, significantly outperforming national averages.

Residential Properties: 95% leased, demonstrating strong demand and operational excellence.

Why Does This Opportunity Exist?

The market may be overlooking CHCI due to its transformation from a capital-intensive homebuilder to a fee-based management company. This transition began in 2018 and was further refined in 2022 with Dwight Schar’s involvement. The company’s micro-cap status and relative illiquidity also contribute to the valuation disconnect.

Risks and Mitigants

Risks:

The biggest risk to this thesis is that management has been overly optimistic about its square footage expansion projections. If there is a market downturn in CHCI's concentrated geographic area (primarily Northern Virginia near Washington, DC), the company may be forced to delay much of its pipeline or, in the worst-case scenario, cancel the buildout altogether. This would significantly impact future square footage growth projections, and consequently, revenue and earnings growth could stall or decline.

Mitigants:

Trophy Properties: CHCI’s portfolio consists of high-quality properties located near metro stations, ensuring strong demand even during challenging market conditions.

Valuation Protection: Even if growth halts entirely today (an unlikely scenario), CHCI would still generate $5.5 million in recurring earnings, and it would be difficult to justify a valuation lower than 11.5x earnings.

This conservative baseline provides downside protection for investors while leaving room for upside if management’s projections materialize.

Conclusion

For an asset-light, fee-based management business run by a highly competent team with a proven track record, CHCI’s current valuation is simply too cheap. Between organic growth, operational leverage, and “free call options” in its model, CHCI represents a compelling opportunity for investors seeking outsized returns in the micro-cap space. With its growth path already in motion and downside protection firmly in place, CHCI offers a rare chance to invest in a micro-cap with asymmetric upside.

Hi Brian, great article - thanks for the write up! Comstock filed a 15-12G to suspend periodic reports (quarterly/annual filings) today. Do you or anyone have opinions into why they would do that? Thanks!

Great writeup.

The termination agreement of the asset management agreement, in my opinion, serves as a very valuable protection to the downside on the value of this business. That being said, given the related party transactions here, is there anything that would prevent CP to amend the agreement to eliminate and/or severely restrict the financial consequences of a termination? There's no specific language that I can come across that speaks to the inability for CP to amend the AMA in their favor.